Andrew Galliers – Transport & Logistics Specialist

When faced with the sheer cost of a lorry, the financially savvy may be more inclined to put such amounts towards projects or investments that generate a return, rather than dedicating funds to a rapidly depreciating asset.

There is a lot of advice floating around about how to finance vehicles including lorries, and it’s not as easy as going for the cheapest option. The choices overlap and multiply, which muddies the waters.

So what are the available finance options?

Let’s start by simply listing the possibilities for making the purchase:

OPTION 1

Buy the lorry outright

OPTION 2

Finance lease

OPTION 3

Hire purchase

OPTION 4

Operating lease

What are your choices for lorry finance?

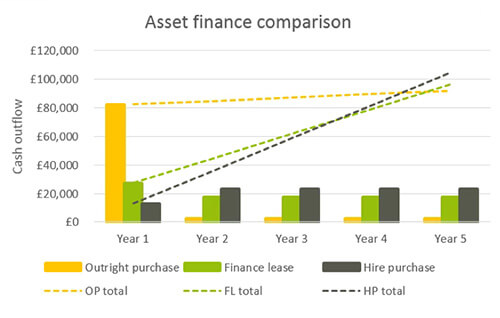

At the end of the day, it boils down to cost. Making a few assumptions about tax rates and ignoring an operating lease for now, we can represent the choices below. The figures, provided by Rangewell, are illustrative. Actual costs and payments will be dependent on the individual circumstances of each company and asset being purchased.

The chart shows the annual payments under each scenario, while the dotted lines illustrate the cumulative amounts. An outright purchase dwarves the initial outlay of the other two, but over five years requires fewer funds. A typical hire purchase plan may put your workers behind the wheel of a lorry at the lowest cost initially, but is it worth it at the final tally? Paying for the lorry in full frees you from the shackles of a leasing company, but is that as valuable as the opportunity cost of diverting say £100,000 into a vehicle that could have gone towards technology that increases the throughput of your assembly line?

Note that the chart reflecting your business’s circumstances may not look like this; we’re merely setting the scene for thinking about a vehicle purchase in the right way.

The choice you make about financing a lorry will produce a future schedule of cash flows that you can put to paper (i.e. a spreadsheet) for a better view on what it will cost you and when. If everything came down to cost, you’d be sorted, but you’ll be asked to make several more decisions.

The decisions

How often would you like to ‘refresh’ your fleet?

How often you wish to refresh your fleet is a critical piece of the puzzle. Is there value for the business in updating the fleet even if everything is working okay? How often? An apparently less expensive leasing agreement may tie you in for longer than you’d like. If you elect to keep the vehicle after the initial hire purchase term, you may well find you’ve got an asset with much lower running costs. On the other hand, when the term of the financing lease is over, you can expect a happy exchange for a new vehicle.

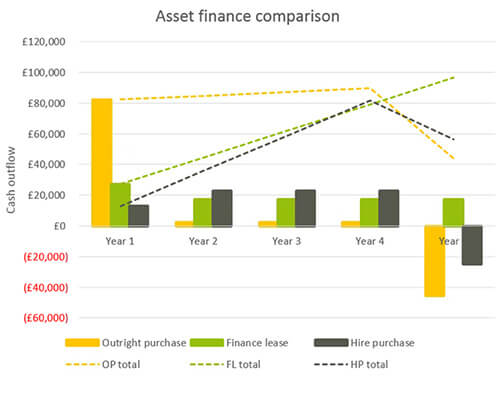

Here’s what things could look like if you sell the lorry after 5 years, which ties into the end of the HP term.

How healthy is your cash flow?

Our chart shows that an outright purchase will mean less cost in the long run, but what if you need a small fleet of lorries? The manageable payment schedule of a hire purchase or financing lease under good terms may pave the way for building a fleet while spreading the costs over the term of the lease. The Financing and Leasing Association cites the popularity of vehicle financing by reporting that £37 billion worth of it took place last year.

The timing of the VAT payment for the lorry can be key for cash flow. Both buying a lorry outright or via a hire purchase will trigger the entire VAT amount on day one. Much of this can be completely reclaimed, but there is a timing delay, and if cash management is a sore point, this may well play into your decision about which way to go. With a financing lease the VAT is included in the monthly payments, so spread out.

What’s the difference in running costs?

This rather crucial consideration has a way of being missed.

Ask yourself: is your business set up to neatly handle multiple unexpected repairs? Do you have the people, time and resources to oversee proper maintenance, or will breakdowns unduly burden the team while it manages the rest of the business?

If maintenance and repairs (or even just their costs) will make you feel edgy, remember that with leases running costs are mainly covered by the lessor company. This is not the case if you own the vehicle, and as for hire purchases, not all agreements are created equally, so check the terms before you sign.

What about the tax relief?

Because your fleet is part of a wider business, you probably don’t want to look at acquiring a truck in isolation. It is important to understand the corporate tax relief and its timing under each option. With a hire purchase or buying the lorry outright, you’ll likely enjoy greater tax relief up front via the super-deduction (available on purchases up until 31 March 2023), which provides relief for up to 130% of the cost. With a finance lease, tax relief is provided as the costs are incurred, so spread over the period of the lease.

The takeaway

Not all arrangements are valid, and attractive lease terms can merely appear that way. If a lorry is part of your business, you’ll be rewarded by doing the hard work now of weighing all the options.

Contact Our Experts